Best International Bank Accounts for Expats & Digital Nomads [2026]

If you’re an American expat living overseas, a digital nomad moving around while working – or simply someone who loves to travel – an international bank account could be a smart way to manage your money.

Some international bank accounts offer ways to hold and exchange foreign currencies, and cut the costs of international transactions. However, international accounts aren’t always available from traditional US banks – and where they are offered, they can come with fairly high fees and restrictive features.

Join us as we walk through some of the best international banks in the US, and also look at some alternatives which can be cheaper and more flexible, like Wise and Revolut.

Best international bank accounts: Quick summary

Before we get started, let’s look at the banks and providers we’ve picked as the top 5 banks for international travel and money management, for expats and digital nomads. We’ve looked at a cross section of options which may suit, depending on whether you want to spend easily when you travel, send payments, or even invest in a selection of currencies from the US.

- Wise account: Great for anyone looking to hold 40+ currencies, spend with a linked debit card in 150+ countries, and receive payments like a local from 30+ countries

- Revolut account: Great for holding 25+ currencies, with a linked card and high levels of no-fee ATM withdrawals, plus tools for budgeting, saving and investing

- HSBC: Global Currency accounts you can manage from your phone, to hold 8 currencies and send payments to your own, and others’ HSBC accounts

- Wells Fargo: Choose the Wells Fargo account to suit your USD money management needs, and add in an international Visa card for spending and withdrawals globally

- Charles Schwab: Best for Schwab customers who want to diversify and invest in foreign currencies without needing to convert back to USD every time

Can you open an international bank account?

Yes. You can open an international bank account in the USA.

- Some traditional US banks offer international bank accounts, although these do tend to have relatively limited features compared to international accounts from specialist services.

- Providers like Wise and Revolut offer online international accounts which can hold multiple currencies and be used easily for everyday transactions.

We’ll look at all of this in more detail a little, next.

5 International bank accounts in the USA

The best international bank account for you will depend on your specific preferences and needs. Here we’ll look at an overview on each provider – and then later we’ll explore more in detail so you can see if any may suit your needs.

Not sure how to pick? Don’t worry. We’ll also cover what to consider when choosing an international online bank.

| Wise account | Revolut account | HSBC Global Money Account | Wells Fargo Everyday Checking | Schwab Global Account | |

|---|---|---|---|---|---|

| Account opening fee | No fee | No fee | No fee | No fee | No fee |

| Account maintenance fees | No fee | No fee for a standard account, upgrade to a monthly fee of up to 16.99 USD to unlock more features | No fee – but you’ll need to also hold another eligible HSBC account, which may have a fee | 10 USD/month, can be waived by hitting eligibility criteria | No fee |

| Multi-currency Account | Hold and exchange 40+ currencies | Hold and exchange 25+ currencies | Hold 7 currencies | Not available – accounts hold USD only | Trade in 7 major currencies |

| Travel Card (debit or credit) | Wise Multi-Currency Card to spend in 150+ countries | All accounts come with linked cards, which can vary based on the plan you choose | No linked card available | Link a Wells Fargo debit card for international use | No linked card available – intended for investment and trading only |

| Foreign Transaction fees | No fee to spend currencies you hold in your account – currency conversion from 0.41% | No fee to spend currencies you hold in your account – all accounts have some no-fee exchange which uses the Google rate | Not applicable – account can only hold, exchange and send payment to other HSBC accounts | 3% | Not applicable – intended for investments and trading only |

| Currency Conversion Rates | Mid market exchange rate – the one you find on Google | Mid-market currency exchange – but this may be capped depending on the account plan. After that, fair usage fees apply, usually 0.5% | HSBC rate will apply, which may include a markup | Visa rate will apply | Charles Schwab rate will apply, which may include a markup up to 1% depending on the transaction value |

| Foreign ATM Transaction Fees | First 2 withdrawals, up to the total value of 100 USD a month with no Wise fees, then 1.5 USD + 2% fee per withdrawals | No-fees applied up to 400 USD/month, 2% fee applies after that | Not applicable | 5 USD per withdrawal, plus any applicable foreign transaction fee | Not applicable |

| International Business Accounts | Both personal and business account plans available | Both personal and business account plans available | This account is for personal customers only | This account is for personal customers only | This account is intended for personal customers looking to trade internationally only |

International accounts can come from banks you’ll know well, or digital specialists which have been built with a great range of international functions, such as Wise and Revolut. Accounts from traditional banks are familiar and reliable but may have rather more restrictive functionality compared to specialist providers.

Here’s a quick reminder of the accounts we’ve looked at:

- Wise account: Hold and exchange 40+ currencies and get paid internationally with local account details from 30+ countries, plus a linked card for everyday spending

- Revolut account: Multi-currency functionality for 25+ currencies, with a selection of account tiers depending on your needs

- HSBC Global Money Account: Hold and exchange 7 currencies, and send payments to other HSBC accounts

- Wells Fargo Everyday Checking: Manage your money in USD, with a linked international Visa debit card, and online overseas transfers with no upfront fee

- Charles Schwab Global Account: Invest in 7 currencies, without needing to convert back to USD every time a payment is made

Let’s look at each provider in more detail now.

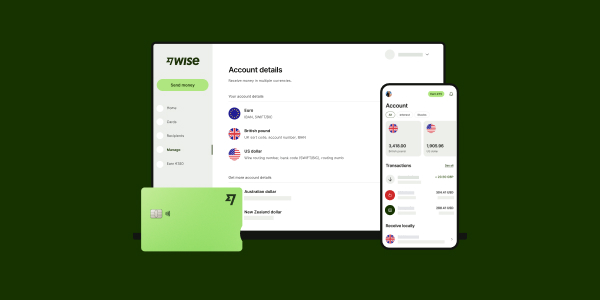

Wise Account – 40+ currencies

💡 Great for: Local account in details in 10 currencies. For people traveling often or shopping internationally, looking for flexible and low cost currency conversion

You can open a Wise account for free, to hold and exchange 40+ currencies and spend with Wise Multi-Currency Card in 150+ countries. You’ll also get local bank details in 10 currencies such as USD, EUR and CAD which makes it easy to get paid from 30+ countries. Plus, you can send money to 160+ countries with Wise fast, with low fees.

Wise uses the mid-market rate for currency exchange – the one you usually find on Google. You’ll only pay a low conversion fee which is from 0.42%, with no fees to spend from any enough currency balance you hold in your account.

- Wise Multi-Currency Card: Order a card for a one time low fee, spend around the world in 150+ countries – and if you don’t have the currency you need the card can convert for you using the lowest possible fee.

- Wise foreign transaction fees: Midmarket exchange rate for currency conversion. Currency conversion from 0.42%, no fee to spend currencies you hold in your account

- International ATM withdrawals: First 2 withdrawals up to a combined total of $100/month for no fee*. After that $1.50 + 2% (once you’ve withdrawn $100 in a given month, any amount in excess will be charged a 2% fee)

You can get local account details in 🇬🇧British Pound (GBP), 🇪🇺 Euro (EUR), 🇺🇸 US Dollar (USD), 🇦🇺 Australian Dollar (AUD), 🇳🇿 New Zealand Dollar (NZD), 🇸🇬 Singapore Dollar (SGD), 🇷🇴 Romanian Leu (RON), 🇨🇦 Canadian Dollar (CAD), 🇭🇺 Hungarian Forint (HUF), and 🇹🇷 Turkish Lira (TRY)

You can hold and exchange money in 40+ currencies including the currencies listed above and 🇯🇵 Japanese Yen (JPY), 🇲🇽 Mexican Peso (MXN), 🇮🇳 Indian Rupee (INR), 🇨🇳 Chinese Yuan (CNY), 🇨🇭 Swiss Franc (CHF)

Learn more: How to get a Wise Multi-Currency Card

Revolut Account – 25+ currencies

💡 Great for: Picking the account tier that suits you, from accounts without monthly fees to fee paying options with extra features- all accounts can hold 25+ currencies

Revolut has a selection of different account plans, from a standard plan you don’t need to pay a monthly fee for, to a full feature account which costs 16.99/USD a month.

Revolut accounts can hold and exchange 25+ currencies and have linked debit cards. You’ll get some currency exchange which uses the Google exchange rate, although the amount you can exchange can vary based on your account plan. Revolut also offers accounts for children and teens under 18, and tools for saving, budgeting and investing.

- Revolut travel card: All accounts have linked debit cards – the exact card you get varies by account tier

- Foreign transaction fees: No-fees applied when spending any currency you hold in your account

- International ATM withdrawals: No-fee withdrawals within network. Up to 400 USD no-fee withdrawals from out-of-network ATMs, even with the standard plan

HSBC, Wells Fargo and Charles Schwab are some of the banks in the US that are international. Let’s take a deeper look into their foreign currency account options, foreign transaction fees and linked cards:

HSBC Global Money Account – 7 currencies

💡 Great for: Existing HSBC customers who need to hold a balance in a foreign currency, or send foreign currency payments to other HSBC customers

HSBC US offers its Global Money Account to customers who already have an eligible HSBC US account, and a local residential address. HSBC Global Money Account is managed via an app and can be used to hold and exchange 7 supported currencies. You can add funds from your own linked HSBC account, convert to the currency you need, and send a payment on to another linked HSBC account easily.

There’s no linked card with this account – although you may have a card linked to the base account you already hold with HSBC. The Global Money Account has no maintenance fees of its own, but you might have to pay a charge to maintain the linked account. There’s also often no fee for sending foreign currency payments – but an exchange rate markup, which is higher at the weekends, will still apply.

- HSBC travel card: No card linked to this account

- Foreign transaction fees: Not applicable – this account can’t be used directly for spending, only to hold a balance and send global payments in the 8 supported currencies

- International ATM withdrawals: Not applicable – no card attached to this account

You can hold and exchange money in 🇦🇺 Australian Dollar (AUD), 🇨🇦 Canadian Dollar (CAD), 🇪🇺 Euro (EUR), 🇬🇧 Pound Sterling (GBP), 🇭🇰 Hong Kong Dollar (HKD), 🇸🇬 Singapore Dollar (SGD), 🇺🇸 US Dollar (USD)

Wells Fargo Everyday Checking – USD only

💡 Great for: Managing your money primarily in USD, but with a linked Visa debit card you can use around the world

Wells Fargo has a broad range of account types, which can all be linked to a debit or credit card for international spending. For this example, we’ve used the Everyday Checking account and the Wells Fargo Visa debit card – one of the lowest cost Wells Fargo accounts available.

You can use your Visa card anywhere you see the Visa logo, with a 3% foreign transaction fee to pay, plus international ATM withdrawal fees if you need to get cash. You’ll also be able to send international wires from your account.

There’s no Wells Fargo fee for international wires initiated online and via the mobile banking service, but an exchange rate markup is likely to apply. If you need to set up your Wells Fargo international transfer in a branch you’ll pay around 35 USD, plus any exchange rate fee, and third party costs as necessary.

- Wells Fargo travel card: You can choose which card to link to your Everyday Checking account, and all cards can be used internationally

- Foreign transaction fees: 3% fee applies

- International ATM withdrawals: 5 USD fee applies

Charles Schwab Global Account – 7 currencies

💡 Great for: Investors who want to trade in up to 7 different currencies (for 12 foreign markets)

If you’re an investor looking to settle payments overseas, and you don’t want to have to exchange to and from USD every time, the Charles Schwab Global Account could suit you. You’ll be able to deposit money into the account from another Schwab investment account, and then switch to the currency you need when it’s time to invest.

This account isn’t really intended for individuals who want to manage their money day to day for travel purposes, so features like a linked debit card aren’t available.

- Schwab travel card: Not available – account intended for investing and trading only

- Foreign transaction fees: Not applicable – no card available

- International ATM withdrawals: Not applicable – no card available

You can hold, buy and sell money in 🇦🇺 Australian Dollar (AUD), 🇪🇺 Euro (EUR), 🇨🇦 Canadian Dollar (CAD), 🇭🇰 Hong Kong Dollar (HKD), 🇯🇵 Japanese Yen (JPY), 🇳🇴 Norwegian Krone (NOK), 🇬🇧 British Pound (GBP)

What is an international bank account?

International bank accounts can have a pretty broad selection of features, from accounts for daily use which let you hold foreign currency balances and get international travel cards, to accounts aimed at international investors.

There are quite a few international banking account options for US customers, although it’s helpful to note that the accounts available from traditional banks can have fairly limited features compared to specialist providers.

We’ll look at some smart options in just a moment – for now, here’s a rundown of some of the features you may get from an international bank account:

- Hold a select of foreign currencies and convert between them

- Send payments overseas with low or no fees

- Access preferential exchange rates

- Spend internationally with a linked debit or credit card

- Invest internationally in foreign currencies

How to open an international account

The process can vary widely for opening a digital bank account offered by a traditional bank, and a multi-currency account like Wise. Some banks may ask you to visit a branch to get started, or you may also need a linked account with the same bank in order to apply for an international account.

In either case you’ll normally need the following documents to open an international account:

- Proof of ID, such as a passport

- Proof of address – which may need to be in the US if you choose a traditional bank

How to open international bank account online

While some traditional banks offer online options for account opening, you may still need to visit a branch or make a phone call to complete the process. With Wise and Revolut the whole process takes place online including verification.

Here’s how to open an international bank account online for free with a specialist provider like Wise or Revolut:

- Download the provider app or head to their desktop site

- Register an account using your email address and add your personal information

- Get verified by uploading images of your documents

- Once your account is verified, you can start using it.

If you need to spend money from your account, you can apply for a debit card. You’ll receive a physical card in the mail, and with some providers you can also create virtual cards as soon as your account is verified.

Learn more: How to open a Wise account

Benefits of international bank accounts

So why bother with an international bank account at all? If you are a frequent traveller, an expat or a digital nomad, international bank accounts can have many benefits. Here are some key advantages to know about:

- Hold and exchange multiple currencies so you don’t need to switch back to USD unnecessarily

- Spend overseas with a linked card – which can mean lower costs and no foreign transaction fees

- Manage your money on your phone with transaction alerts and an instant overview of all your currency balances

- Open local receiving accounts to get paid easily and with no or low fees, in a selection of currencies

How to choose the best international bank account for your needs

There’s no single best international account, so you’ll need to review a few, looking at features and fees, to pick the one that suits you best.

Here are a few key points to consider when choosing the right account for you:

- Availability of foreign currencies: Check that currencies you use frequently are supported for holding, exchange and spending

- Monthly charges: Accounts are available with no monthly fees – although you may also choose to upgrade to an account with a maintenance charge to get more features

- International fees: Check for foreign transaction and foreign cash fees, and ATM charges when you travel – these can mount up steeply depending on the account you select

- Currency conversion rates: Ideally look for an account which uses the Google exchange rate with no hidden charges. This is transparent and makes it easier to assess what you’re actually paying for overseas transactions

- International travel cards: If you’ll be traveling it’s worth checking you’ll have a linked debit or credit card, issued on a major global network

- Overseas money transfers: See how much you’ll pay to send money overseas, and how many countries are available for transfers – handy for sending payments to friends and family or covering overseas bills

- Ease of use: Choose an account with easy mobile and online access, so you can use your account wherever you are

- Extra features: Different accounts have their own features, like investment options and local bank details to get paid for free from overseas

- Safety: Finally, pick a reputable provider which is licensed and regulated in the US and internationally

What are the best international banks with no fees?

It costs to offer international services. That means that while some banks may look like they have no fees, the chances are that they’ll have transaction and service fees, and exchange rate markups which can be tricky to spot.

Here is fee the structure of the providers we’ve explored in this article:

- Wise fees: Accounts are free to open, there is no maintenance fee, there are low transaction fees. Plus, Wise currency exchange uses mid-market exchange rate.

- Revolut fees: Standart accounts don’t have an opening fee, there are different packages with varying monthly fees including a standard plan that is 0$/month.

- HSBC international fees: No fee for the Global Currency account, but you’ll need a linked account which may have its own charges

- Wells Fargo foreign fees: 10 USD/month for Everyday Checking account, plus transaction and service fees like a 3% foreign transaction fee

- Schwab foreign fees: No account fee, but you’ll pay transaction charges and currency fees when you trade

What is the safest international bank?

All of the providers we feature on Exiap are regulated and licensed providers, with industry level security measures. Here’s a look at how the providers we have featured which offer international spending keep you safe when you spend:

- Is Wise?: Get transaction alerts in the app, freeze and unfreeze the card easily when you travel

- Is Revolut safe?: Manage your account in the app, including viewing balances and transactions

- Is Wells Fargo safe?: Access online and mobile banking to keep on top of your account when you’re away

Best ways to withdraw money when traveling abroad

Sometimes you can’t manage with digital payments and need to get some cash. Here are some ways to cut the costs of cash withdrawals overseas:

- Always check your banks foreign transaction fees so you know if you’ll pay a premium when abroad

- Check which ATMs you can use for no extra fee when you travel – providers like Wise and Revolut offer some no-fee international withdrawals every month

- Always withdraw in the local currency wherever you are, to avoid dynamic currency conversion

- Avoid withdrawals with a credit card as these have extra fees

How to avoid foreign transaction fees

But what about when you spend with your card overseas? Here are some ideas to keep down costs:

- Check your bank’s foreign transaction fees and exchange rates – you may be better off with a specialist like Wise or Revolut

- Pay in the local currency to avoid dynamic currency conversion

- Look at multi-currency accounts from Wise or Revolut to keep your money in local currencies to avoid paying high conversion fees with bad exchange rates

Conclusion: Best banks for international travel

There are a few different options for international accounts for expats – either from traditional banks or specialist online services.

Traditional bank options can be somewhat limited, with a focus on payments and investing rather than day to day spending. As an alternative, look at specialists like Wise and Revolut, which can be handy for easy everyday use, and to hold a broad range of currencies all in the same place.

FAQs: Best banks for digital nomads and expats

Can you open an international bank account online?

Some traditional banks offer international online banking accounts – but you’ll normally already need to be a customer to apply. Alternatively, look at specialists like Wise and Revolut, for online onboarding and verification.

What are the best international banks with no fees?

All banks and financial service providers have some fees – it’s just that these may not be easy to spot with some account options. Look for an account with a provider which is transparent about charging, so there are no surprises.

Which bank account is best for international travel?

There’s no single best account for international travel, but an account which lets you hold multiple currencies and spend with a linked debit card can help you cut the costs of currency conversion and international spending. Check out Wise and Revolut for some great online international account options.

How can you avoid bank charges when traveling internationally?

Double check your own account’s terms and conditions carefully before you head overseas, looking for foreign transaction fees and international ATM costs. You may find you’re better off with an online international account for when you’re abroad.

What bank does not charge international ATM fees?

Your own bank may have some no-fee international ATM options with partner banks – or you can check out options like Wise and Revolut which both offer accounts with some no-fee overseas ATM withdrawals every month.

Should you have a separate bank account for travel?

It’s not entirely necessary to have a separate account for travel, but it can help you manage your budget, and add an extra layer of security. Pick a provider like Wise and Revolut and you may also get more transparent fees and a better exchange rate compared to your bank.