10 Best Multi-Currency Accounts in the US [2026]

Opening a multi-currency account is advantageous for those dealing with international transactions, such as paying bills abroad, receiving payments from overseas clients, or managing foreign currency payments.

While some major US banks offer multi-currency accounts, they may lack flexibility and come with high costs. Specialist providers like Wise and Revolut can be good alternatives.

In this guide, we’ll look at 6 multi-currency bank account options from US banks, as well as 4 online specialists that are available for US residents.

💡 Overview: Best multi currency accounts in the US 💱

First, a quick look at some of the key US multi-currency account providers we’ll explore:

| Multi currency bank accounts | Great for: |

|---|---|

| Wise account | Personal and business accounts with 40+ currencies, local account details in 8+ currencies. Mid-market exchange rate with low and transparent fees |

| Revolut account | Hold and exchange 25+ currencies, and get some international ATM withdrawals and conversion without additional fees |

| Payoneer account | Accounts for digital business owners and e-commerce sellers, to pay and get paid in foreign currencies |

| OFX Global Business Account | For business customers only, with 30 hold currencies. Payments and currency risk management solutions with 24/7 phone support available |

| Wells Fargo foreign currency bank account | Allows businesses to receive payments in foreign currencies, for corporate customers only |

| Chase Commercial Banking international services | International services tailored to large enterprise level organizations |

| Citibank foreign currency account | Offers foreign currency accounts through Citi Private Bank, very high minimum balance requirement |

| HSBC Global Money account | Existing HSBC US customers can open a Global Money account to hold and exchange 8 currencies with preferential rates |

| Everbank / TIAA Bank multi currency bank accounts | Accounts and Certificates of Deposit in single currencies or a basket of foreign currency options |

| East West Bank multi currency bank account | Traditional Demand Accounts and Certificates of Deposit in major foreign currencies |

Table of Contents

- 💡 Overview: Best multi currency accounts in the US 💱

- What is a multi-currency account?

- 🌍 Best multi-currency accounts in the US 🏆🇺🇲

- Best multi currency bank accounts 🏦

- 🏦 Which US banks offer foreign currency accounts?

- How to open a foreign currency account online

- When is a multi-currency account needed?

- What is the eligibility for a multi currency bank account?

- How to choose the right foreign currency account for your needs

What is a multi-currency account?

A multi-currency account can be useful for individuals who live an international lifestyle, freelancers and online sellers getting paid from abroad, and businesses who trade around the world.

Being able to get paid in foreign currencies, hold multi-currency balances, and send money overseas without needing to convert the currency can cut your costs.

🌍 With a multi-currency account you can hold various currencies in one place other than US dollars, including the following most popular: Pound Sterling (GBP) 🇬🇧, Euro (EUR) 🇪🇺, Canadian Dollar (CAD) 🇨🇦, Australian Dollar (AUD) 🇦🇺, Hong Kong Dollar (HKD) 🇭🇰, Japanese Yen (JPY) 🇯🇵, and Singapore Dollar (SGD) 🇸🇬. Some accounts also support USD so you can top-up easily and convert to other currencies conveniently.

| Pros of multi currency accounts | Cons of multi currency accounts |

|---|---|

| ✅ Flexibility: Hold and transact in multiple currencies ✅ More favorable exchange rates: Take advantage of more favorable rates ✅ Low conversion fees: Save money on currency conversion ✅ Convenience: Make easy international transactions | ❌ Limited availability: Not all banks offer these accounts, leaving specialist providers ❌ Complexity: Can be more complex to manage compared to a single currency account ❌ Fees and charges: Some accounts may have high fees ❌ Low or no interest rate: Not all multi currency bank accounts offer interest on foreign currencies |

💡 Here are some of the frequently asked questions, and answers:

| Questions | Answers |

|---|---|

| Which US banks offer multi currency accounts? | A few US banks offer multi currency bank account options, like East West, HSBC, and TIAA, while Chase, Bank of America and Wells Fargo offer foreign currency bank accounts for business customers only. |

| How can I open a foreign currency account in the US? | Many accounts can be opened online or through a provider app – but you’ll probably need to pop into a branch to get an account through a bank. With Wise and Revolut, you can open an account online. |

| How does a foreign currency account work? | Foreign currency account features vary – you’ll usually be able to to hold and exchange foreign currencies, send and receive payments internationally. |

🌍 Best multi-currency accounts in the US 🏆🇺🇲

Ultimately, the best multi-currency account for you will depend on your specific needs and personal preferences. To help you pick, let’s look at an overview of some of the most popular foreign currency and multi-currency accounts in the US. We’ll start with the accounts you can open from specialist and alternative providers:

| Provider | 🇺🇲 Availability | 💰 Monthly fee | 📥 Min. balance | 🌍 Currencies | 💳 Debit card |

|---|---|---|---|---|---|

| Wise | Available for business and personal customers in many countries | No fee | No minimum balance | 40+ currencies | Available |

| Revolut | Available in a range of countries including the US, UK, EEA and Australia | No monthly fee for standard account – up to 16.99 USD for Metal account | No minimum balance | 25+ currencies | Available |

| Payoneer | Available in a range of countries | Free – an annual fee applies for low use accounts | No minimum balance | 7 currencies | Available |

| OFX | Business customers only | 15 USD – 25 USD per user per month | No minimum balance | 30 currencies | Available |

*Details correct at time of research – 26th February 2026 *About Wise pricing: Please see Terms of Use for your region or visit Wise Fees & Pricing for the most up to date pricing and fee information.

Best multi currency bank accounts 🏦

Next, let’s take a look at the foreign currency accounts you can open from banks in the US. It’s useful to know that most foreign currency accounts from banks are aimed at particular target customers, such as high wealth individuals looking to invest, or businesses which need to manage international payments.

| Foreign currency bank account | 🇺🇲 Availability | 💰 Monthly fee | 📥 Min. balance | 🌍 Currencies | 💳 Debit card |

|---|---|---|---|---|---|

| Wells Fargo | Business customers only | Services are tailored to client needs | Services are tailored to client needs | 28 currencies | Contact bank directly |

| Chase | Business customers only | Services are tailored to client needs | Services are tailored to client needs | Services are tailored to client needs | Contact bank directly |

| Citibank | High wealth individuals | Varied fees based on account type | Assets of 5 million USD+ | Not specified | Available |

| HSBC Global Money Account | HSBC customers with eligible accounts only | No fee | No fee | 8 currencies | Not available |

| Everbank / TIAA Bank | US residents | Based on account type | 2,500 USD | 20 currencies | Not available |

| East West Bank | US residents | Based on account type | Not specified | 14 currencies | Not available |

*Details correct at time of research – 26th February 2026

Methodology: To determine the best multi-currency accounts in the US, we compared US banks against specialist providers based on their suitability for personal and business international transactions. Our evaluation focused on critical factors like the number of supported currencies, exchange rates, and the impact of fees. All data was verified through primary provider documentation as of late February 2026 to ensure accuracy.

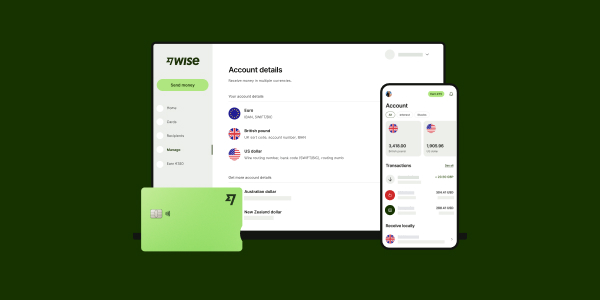

Wise multi-currency account – 40+ currencies

You can open a Wise multi-currency account online or in the Wise app, with options available for business and personal customers.

There are no ongoing fees to pay and no minimum balance to maintain, so you can use the account as and when you need it, to access currency exchange which uses the mid-market exchange rate and low, transparent transaction fees.

Order a linked Wise Multi-Currency Card for a one time fee, to spend and make withdrawals in 150+ countries, hold 40+ currencies in your account, send payments to 140+ countries, and get paid with account details for 8+ currencies.

| Wise account features & pricing | |

|---|---|

| 🌍 Foreign currencies | 40+ currencies supported for holding and exchange |

| 📂 Account details | Receive with local account details in AUD, CAD, CAD, EUR, GBP, HUF, NZD, SGD, TRY, USD |

| 💰 Wise account fees | Low transaction fees based on services required – no ongoing fee

|

| 🏦 Eligibility | Apply with proof of ID and SSN or ITIN from the US |

| 💱 Wise exchange rates | Live mid-market exchange rate |

| 🔐 Is Wise safe to keep money in? | Yes. Wise has high level account security features and strong anti-fraud measures in place |

| ➡️ International money transfers | Send to 140+ countries, with fees from 0.57% |

*About Wise pricing: Please see Terms of Use for your region or visit Wise Fees & Pricing for the most up to date pricing and fee information.

➡️📚 Learn more: Wise Account Review & How to use Wise Account ⬅️

Revolut multi-currency account – 25+ currencies

Revolut offers services to individuals and businesses in the US and a range of other countries. All accounts offer a linked Revolut debit card.

There are standard Revolut plans without monthly fees available for all customers, which come with the option to hold and exchange 25+ currencies and get a linked debit card for easy spending.

If you want to access an even broader range of features you can also choose to pay a monthly fee of up to 16.99 USD as a personal customer, to get lifestyle perks and more no-fee transactions.

| Revolut account features & pricing | |

|---|---|

| 🌍 Foreign currencies | 25+ currencies supported for holding and exchange |

| 📂 Account details | Local account information for USD and GBP, SWIFT details for other currency payments |

| 💰 Revolut account fees | 0 USD – 16.99 USD monthly fees for personal customers, all accounts have some no-fee currency exchange which uses the Revolut exchange rate |

| 🏦 Eligibility | US residents can apply online or in app with their ID and personal details |

| 💱 Revolut exchange rates | Revolut exchange rate. Fair usage fees apply when you hit the exchange limits on your plan |

| 🔐 Is Revolut safe to keep money in? | Yes. Revolut has strong security measures and thorough verification processes |

| ➡️ International money transfers | 0.15% for transfers sent in the local currency of the destination country |

OFX multi-currency account (business customers only) – 30 currencies

OFX is a currency specialist which has multi-currency accounts for business owners and online sellers.![]()

You can get local bank details to get paid by clients in 4 foreign currencies, or withdraw from PSPs and marketplace sites easily, and can hold a balance in 30 currencies.

Hold or exchange your funds, or use them to pay VAT and suppliers overseas. OFX has a 24/7 phone service for customers which can be helpful if you’d rather talk through your options before transacting.

Corporate cards are available to make business expense spending easier.

| OFX Global Business Account features & pricing | |

|---|---|

| 🌍 Foreign currencies | 30 currencies supported for holding and exchange |

| 📂 Account details | Local account details in 4 foreign currencies |

| 💰 OFX account fees | 15 USD – 25 USD per user per month |

| 🏦 Eligibility | US registered business owners – apply online or in app |

| 💱 OFX exchange rates | Rates may include a small markup |

| 🔐 Is OFX safe to keep money in? | OFX is a safe and well liked provider with good in built security and a 24/7 phone line if you need help |

| ➡️ International money transfers | Send to a range of countries – no transfer fee |

Payoneer multi-currency account – 10 currencies

Payoneer offers online and in-app account services for ecommerce sellers, people who run digital businesses and anyone earning from a third party site like a marketplace or vacation rental portal.![]()

You can get paid with local receiving accounts in a range of 10 currencies, and get a linked card if you want to spend and make withdrawals directly.

Payoneer also offers extra business services to support freelancers and SME owners in the US such as working capital and access to providers who can support you in growing your operations.

| Payoneer account features & pricing | |

|---|---|

| 🌍 Foreign currencies | 10 currencies supported for holding and exchange |

| 📂 Account details | Receive payments from others in 10 currencies |

| 💰 Payoneer account fees | No ongoing fees unless your account is used very infrequently – other transaction fees can apply which depend on account usage |

| 🏦 Eligibility | Freelancers and registered business owners in the US |

| 💱 Payoneer exchange rates | Exchange rates include a markup of 0.5% |

| 🔐 Is Payoneer safe to keep money in? | Yes. Payoneer has strong encryption and automatic and manual anti fraud protocols running to keep your money safe |

| ➡️ International money transfers | Variable fees depending on currency and your account usage |

Learn more: Payoneer review

🏦 Which US banks offer foreign currency accounts?

Unfortunately popular banks such as Wells Fargo, Chase and Bank of America don’t provide foreign currency bank accounts for personal banking, their foreign currency accounts are for business customers only.

There are a couple US banks that offer multi-currency bank accounts for personal users.

Here, we’ll give an overview of HSBC, TIAA, East West personal multi-currency account options, and also Wells Fargo and Chase for business accounts.

💡 Keep in mind that this is not a complete list, and there might be other banks that provide foreign currency accounts in the US.

Wells Fargo foreign currency account (Business customers only)

Wells Fargo offers international treasury management services, and multi-currency account services to corporate business clients.![]()

These services are operated through offices based in Europe and Canada and allow business customers to receive foreign currency payments, and accumulate foreign currency deposits with one institution.

As services are tailored to business needs, the features and fees available can vary widely. Contact Wells Fargo directly for advice

HSBC Global Money Account – 8 currencies

HSBC is a big global banking brand which supports US personal customers with an option to get a multi-currency account to hold and exchange 8 currencies and make payments to others.![]()

You’ll need to have another HSBC account product to access your Global Money Account – and once you have it all set up you can access competitive FX rates and instant payments in a range of currencies to other HSBC customers.

There’s no monthly fee, but you do have to hold another eligible HSBC account which may have a maintenance charge.

Check our review here: HSBC Global Money Account review

Chase Commercial International banking

Chase does not offer a foreign currency account for personal customers, but does target business customers with a broad range of international services.![]()

In particular, Chase works with businesses in sectors like healthcare, finance, retail and real estate which are likely to have high annual turnovers, and complex international banking needs.

Chase services for commercial businesses are tailor made to suit the needs of the individual organization. To learn more about what’s available – and whether Chase might be able to help you with your own business requirements – you’ll need to complete an online form and wait for a call back.

Citibank international services (from Citi Private Bank)

Citibank offers international services to customers who maintain a high minimum relationship balance. These accounts allow customers to access detailed investment advice and favorable fees for foreign exchange services.

Citibank USA doesn’t offer a multi-currency account, but they can refer you to Citi Private Bank, which requires a minimum assets under management of 5 million USD.

TIAA Access Accounts (now Everbank) – 20 currencies

TIAA has Access Accounts for day to day use which you can hold in foreign currencies, as well as Certificates of Deposit (CDs) in single currencies or a basket of foreign currency options.

![]()

CDs may be a good option if you want to boost your savings in a foreign currency and don’t mind locking away your funds for a fixed period in order to get the best available rate of return.

20 currencies are supported for holding and exchange. Fees and rates vary by currencies involved and minimum balance requirements may apply.

East West multi currency bank account – 14 currencies

Get Demand Accounts and Certificates of Deposit in 14 major foreign currencies from East West. There’s a pretty good range of currencies and you’ll get a better exchange rate with this account than you may otherwise with East West.

No minimum balances apply, but you may need to pay a monthly fee depending on the account and currencies you select.

Fees and rates vary by currencies involved. Bear in mind that although you can use international transfers to send money to a range of countries, there’s no multi currency debit card with this account.

How to open a foreign currency account online

Exactly what you need to do to open a multi-currency account in the US will depend on whether you choose a bank, digital or specialist provider.

Many accounts can be opened online or through a provider app – but keep in mind that you might need to pop into a branch to get a foreign currency account through a US bank.

📲💡 Here is how to open a multi-currency account online: 🌍

- Choose the best provider for your needs

- Check you meet any eligibility criteria

- Register for your account online, or through the provider app

- Give your personal and contact information

- Complete the required verification steps

- Fund your account – and you’re ready to go

US legislation means that all banks and account providers must complete verification steps to make sure that customers don’t use their products fraudulently or illegally.

That means you’ll usually have to provide some paperwork in person or by uploading an image when you choose a digital account provider.

Usually the documents you’ll be asked for verification are:

- Government issued photo ID to prove your identity

- Proof of address – a utility bill or bank statement in your name for example

- Business registration documents if you’re opening a business account

If you are interested in a specific currency account, these guides might help:

- How to open a Canadian Dollar account in the US 🇨🇦

- How to open a Euro account in the US 🇪🇺

- How to open a British Pounds account in the US 🇬🇧

Free multi currency bank accounts

There are always some costs involved with managing your money, which could take the form of ongoing charges or transaction fees. However, there are some multi-currency accounts from banks and specialist providers which do offer some services with no fees.

These can be a good option if you’re not sure how frequently you’ll use your foreign currency account, or if you just want a low risk way to test out the accounts on offer.

Different banks and specialist alternatives have their own approaches to fees. Some may offer you a fixed number of free transactions before any charges begin for example, while others may offer multi-currency features you can access as long as you hold a minimum deposit.

Here are a few to consider:

- Wise account: No fee to open a personal account, no ongoing charge or minimum balance, some ATM withdrawals monthly with no Wise fees*, and low, transparent charges where costs apply

- Revolut account: Choose a standard account with no ongoing fee, or pay monthly for more features. All accounts have some no-fee currency conversion and ATM use before charges begin

- HSBC Global Money: No fee for your Global Money account, although you’ll also need another eligible HSBC USD account which may have costs attached

*Wise will not charge you for these withdrawals, but some additional charges may occur from independent ATM networks

When is a multi-currency account needed?

Multi-currency accounts let you hold and exchange a range of currencies, which can be handy for both personal and business customers.

Holding foreign currencies can cut the costs of currency exchange if you get paid from abroad, or if you need to send money internationally often.

If you pick a multi-currency account from a specialist service you may also get a linked international debit card for low cost withdrawals and spending overseas, as well as local bank details to get paid like a local from a range of countries.

How do multi currency accounts work?

Account features do vary depending on the provider you select, but if you pick a modern provider with flexible account options you can often do the following with your multi-currency account:

| Description |

|---|

| 📥 Top up your account in USD or a foreign currency from your bank or card |

| 📲 Check your balance and review transactions on your phone – often with instant transaction alerts |

| 💳 Manage your card – freeze and unfreeze – on the go in the provider app |

| 💱 Exchange currencies within your account |

| ➡️ Send payments to others to be deposited into their bank accounts |

| 🏧🛍️ Spend with your linked debit card, all around the world |

| ⬇️ Receive payments with local bank details |

Multi currency debit cards

Multi currency accounts like Wise and Revolut have linked debit cards that allow you to spend from the account. If you’re interested in a multi currency card, these guides might be helpful:

What is the eligibility for a multi currency bank account?

Multi-currency accounts with US banks are usually aimed at corporate and large business customers which need a full suite of financing and treasury services.

As a result they may have relatively high fees and minimum balance requirements, plus strict eligibility restrictions which make them unsuitable for individuals and small business owners.

Multi-currency and foreign currency accounts from modern alternative providers are chosen by both personal, business and enterprise level customers.

Depending on your needs, these specialist services can offer greater flexibility, lower fees and more convenience compared to the options available from many big US banks.

How to choose the right foreign currency account for your needs

Before you pick a multi-currency bank account, it’s worth comparing a range of options, and looking carefully at both the features and the fees of each. Consider:

- Are the currencies you need covered?

- What are the ongoing fees and charges?

- How high are transaction fees for the transactions you’ll need to make often?

- Can you get a linked debit card?

- Do you get local bank details to get paid easily in foreign currencies?

- What security measures are in place?

➡️💡 Related: Best ways to receive money from overseas

Conclusion: What is the best foreign currency bank account?

As more people travel, work and trade internationally, multi-currency accounts are becoming more popular with both personal and business customers.

Holding a range of currency balances can mean you spend less on unnecessary currency conversion, and can pay and get paid more easily in foreign currencies.

The choice of multi-currency accounts in the US from banks can be limited – and the features, flexibility and fees do vary significantly. Alternative providers like Wise and Revolut can be a good option for both personal and business needs, with easy account opening processes, low fees and great exchange rates.

Make sure you do a bit of research before you get started to find the best match for your needs from the US banks, online and specialist providers out there.