How to Open an International Bank Account in 2026

Looking to open an international bank account? Whether you’re planning to move to a different country or you need to make regular transfers abroad, managing your money across different countries and currencies can be challenging.

In this article we’ll look at how to open an international bank account with a bank or online specialist service, including the documents you need. We’ll also analyze the best options available to show you some of the most cost-effective international accounts, such as Wise or Revolut. But more on that later, read on.

How to open an international bank account

The exact steps you need to take to open an international account will vary based on the provider you pick. Banks often ask you to visit a branch to get your account set up and provide your paperwork for verification. Digital specialist services will allow you to complete the entire process from home, usually with nothing more than your phone to upload your documents.

Here’s how to open an international account step by step:

Step 1. Choose the bank or provider you prefer

Doing some research to find the right bank and account type is essential. Take a look at the international accounts on offer from some of the big global banking brands available in the US, as well as digital specialist services like Wise and Revolut.

- Wise: For anyone looking to hold 40+ currencies, spend with a linked debit card in 150+ countries, and receive payments like a local from 30+ countries

- Revolut: Holding 25+ currencies, with a linked card and high levels of no-fee ATM withdrawals, plus tools for budgeting, saving and investing

- Charles Schwab: US multinational bank known for its investor-friendly approach, offering international banking services with perks for travelers.

- HSBC: A global banking giant providing a range of international account options suitable for cross-border banking needs.

But more on these providers later on.

Step 2. Fill in the application in a branch, via an app or online

Complete the application form online or in hard copy, and start to gather the paperwork and evidence you might need to support your application. Application process could vary from provider to provider.

Step 3. Provide the necessary documents

All banks need to follow verification processes, so you’ll have to provide documents either by scanning and uploading them if you can apply online, or by visiting a bank branch. Common documents typically include a passport or driver’s license as well as proof of address like a utility bill to verify your identity, which is essential for any bank application process.

Step 4. Fund the account

Depending on the account type you choose you may now need to add a fixed minimum deposit to get started. While this isn’t required by all providers, it’s common to add a small amount to your account to start using it and gain access to all of its features. Wise, Revolut., Charles Schwab Global Investing Account and HSBC’s Global Money Account don’t impose a minimum deposit requirement, making them a great choice for anyone looking for a low-cost option.

Step 5. Start using the account

Once your account has been verified – which can happen instantly, or may take a day or two – you’re ready to start using your account. You’ll be able to set up online or mobile banking, order a bank card and begin to manage your international account in your preferred way.

What do you need to open an international account?

Exactly what’s needed to open your account will depend a lot on the provider you select. It’s a good idea to double check before you start your application, so you’ll know you have all you need to hand.

Here’s a rundown of the documents often needed to open an international account:

- Proof of identity – a passport, driving license or other government issued photo ID

- Proof of address – a utility bill or government correspondence in your name, usually from within the last few months

- Proof of minimum funding or salary, depending on the eligibility requirements for the account

Can you open an international bank account online for free?

Yes, you can open an international account online without paying account opening fees.

- Some banks will let you open an international account online – but this isn’t always an option with a bank. Account opening is usually free with banks, but there might be a minimum deposit amount to open the account.

- Digital providers like Wise and Revolut offer online application, verification and onboarding processes. Plus, you can open an account without paying account opening fees, and there is no minimum account balance requirement.

What is an international account?

An international account lets you hold one or more foreign currencies, and make easy payments internationally. While different providers have their own features and fees, accounts can often come with linked cards for payments and withdrawals, and ways to pay and get paid in foreign currencies.

Here’s a quick overview of some of the people who may benefit from an international account:

- Anyone who travels internationally for work or leisure

- People who split their time between countries, like snowbirds who need a way to manage USD and CAD side by side

- International students and expats living away for work

- Travelers to Europe who need a Euro non-resident account

- Freelancers and contractors getting paid in foreign currencies

- Business owners looking to send and receive overseas payments

- People who choose to invest in foreign currencies or assets

Depending on the international account you select, you may find it’s easier to send and receive foreign currency payments, and hold multi-currency balances. That means you can send international money transfers without the need for currency conversion, bringing down the costs overall.

Can I open an international bank account from the US?

Yes. You can open an international bank account in the US, either with a bank or a digital provider like Wise or Revolut.

There’s not a huge selection of multi-currency accounts on offer from mainstream banks, particularly if you’re a personal customer looking for a day to day international checking account.

Banks do tend to have a broader selection of services for businesses and customers looking to invest, though. We’ll cover more on these options in the following sections.

Who is the international bank account for?

International bank accounts can be handy for people moving to a different country for a limited time to work or study, people transferring money in different currencies, and people receiving salaries in different currencies.

If you pick an account which offers multi-currency balances and a linked payment card you could also find it’s handy for any international travel, and even when shopping online with retailers based overseas.

Different providers have quite different account options which suit different customer needs. It’s worth noting that international accounts from banks often come with strict eligibility requirements such as minimum balance or salary levels, and monthly fees.

However, in exchange you can often access wealth management services, rewards and priority treatment. Digital services can be more flexible with lower overall costs – we’ll look at a comparison of some banks vs specialist services, later.

More information: Best international bank accounts

Benefits of international bank accounts

An international account is a valuable resource for people who travel frequently, or who are living abroad for work or study. International accounts are also helpful for freelancers, and online sellers who receive payments from overseas, as well as businesses that engage in global trade.

Here are some of the key benefits of an international account:

- Spend conveniently when you travel or shop in foreign currencies – particularly if you have a multi-currency account which lets you hold a selection of currencies

- Lower fees and better exchange rates when you send a payment overseas or spend using your linked card

- Receive foreign currencies – useful if you’re an international freelancer or business owner getting paid from overseas

- Hold foreign currencies for future use, to pay overseas bills, or to invest

| 💡 Good to know |

|---|

| Multi-currency accounts with a linked card can mean you cut out foreign transaction fees when you travel or shop online in foreign currencies – saving around 3% compared to using many normal bank cards |

4 Best international bank accounts

Not sure where to start? We’ve got you covered. In this section, we’ll cover 4 providers that offer international accounts, such as online specialists like Wise and Revolut as well as banks like Charles Schwab and HSBC.

| Services offered | Wise account | Revolut account | Charles Schwab Global investing account | HSBC Global money account |

|---|---|---|---|---|

| Foreign currencies supported | 40+ currencies | 25+ currencies | 7 currencies | 7 currencies |

| Local account details | Yes – in 10 currencies including USD, GBP, and EUR | USD local account GBP local account | No | No |

| Account opening fee | No fee | No fee if you opt for the standard plan | No fee | No fee |

| Minimum balance requirement | None | None | None | None |

| Maintenance fees | None | Monthly fees dependant on your chosen plan from $0-$16 per month | None | None |

| International transfers | Send payments to 160+ countries | Send payments to over 150+ countries International transfer fee from 0.3% once no-fee transactions are exhausted | Trade in international securities in more than 30 countries 15 USD when arranged online + any applicable currency conversion fee | Send 19 currencies to 20+ countries Free – to HSBC accounts only |

| Currency conversion | From 0.42% Mid-market exchange rate | Currency conversion fee of 0.5% – 2% once no-fee conversion is exhausted Mid-market exchange rate | Conversion fee from 0.2% – 1% | No currency conversion fee transfer to another eligible HSBC customer Exchange rates may include a markup |

| International debit cards | 9 USD order fee | No-fee with your chosen plan | Debit card not available | Debit card not available |

The accounts available from digital providers like Wise and Revolut tend to be more designed for day to day use, with linked multi-currency cards and easy ways to pay and get paid.

Banks which offer multi-currency or foreign currency account services often have more of a focus on customers who want to invest in foreign currencies, and high wealth individuals who want additional perks and services.

Here’s a summary of the international account providers we’ve picked out:

- Wise account: hold and exchange 40+ currencies, get local bank details for 10 currencies to get paid easily, send money to 160+ countries and use your linked Wise Multi-Currency Card in 150+ countries

- Revolut account: hold and exchange 25+ currencies with some no-fee currency exchange included for all account types, plus linked international debit cards, budgeting, investment and saving features

- Charles Schwab Global Investing Account: invest in 7 major currencies and 12 of the top-traded foreign markets, with real time quotes, multi-currency reporting and no trade minimums

- HSBC Global Money Account: hold and exchange 7 currencies, from the HSBC app. Exchange with preferential rates, and send to your own or others’ HSBC accounts for free

We’ll cover each providers’ account in more detail, next.

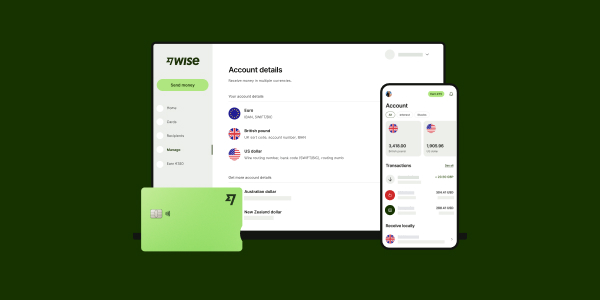

Wise account

You can open a Wise account online or through the Wise app, and are a good choice for day to day money management across currencies.

You can hold 40+ currencies, send payments to 160+ countries, and get local bank details to get payments easily in up to 10 currencies. Wise accounts also come with the option to get a Wise Multi-Currency Card which can be used for spending and withdrawals in 150+ countries.

Best features of the Wise account:

- No monthly or annual fees to pay and, no minimum balance requirement

- Hold and exchange 40+ currencies

- Local account details in 10 currencies to get paid like a local from 30+ countries

- Currency exchange uses the mid-market rate with low fees from 0.42%

How to open a Wise account

Opening a Wise account is easy and convenient. Register via the Wise app or website by clicking the ‘Register’ button and add your email address. You can also sign up using your Google, Facebook or Apple account and you’ll need to verify your identity with documents like your passport or driver’s license. Once verified, you can set up your payment and open a currency balance.

Eligibility to open an account: Opening an account with Wise is easy and you can register online in minutes. You’ll need to be at least 18 years old and provide your legal name, date of birth, and address. For business accounts you’ll need your business tax ID and registration address.

| Pros of Wise account | Cons of Wise account |

|---|---|

|

|

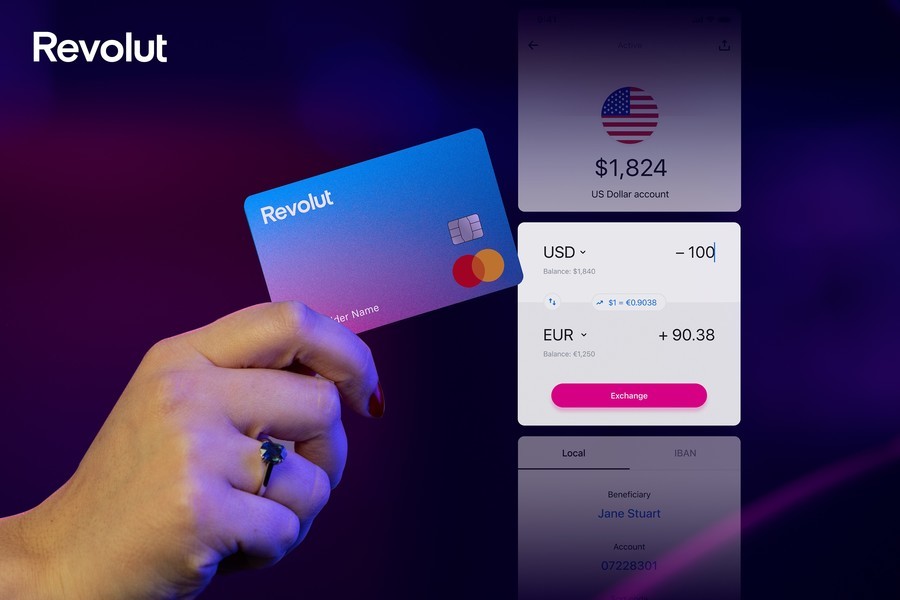

Revolut account

Revolut customers can open an account in the Revolut app, and hold 25+ currencies. Revolut has a selection of account plans, from the standard account which has no monthly fee but also comes with more limited features and no-fee transactions, to premium tier accounts which have higher fees but a broader selection of services available.

All Revolut accounts have linked cards for payments and withdrawals around the world, plus some no-fee currency exchange, based on the account type you pick.

Best features of the Revolut account:

- All accounts have some no-fee currency conversion included

- No-fee ATM withdrawals within plan limits, 2% fees after that

- Hold and exchange 25+ currencies

- Earn interest on your balance

How to open a Revolut account

Download the Revolut app to open an account and enter your phone number to receive a 6-digit verification code. You’ll then need to add your personal details, including your name, birth date, address and email and verify your identity with a photo of a government-issued document and a selfie. Once you’ve been verified, you can choose your plan and start using your account.

Eligibility to open an account: To open an account with Revolut you’ll have to be over 18 years of age and meet verification requirements. They also offer a junior account for teens aged 13 and above with parent or guardian approval.

| Pros of Revolut account | Cons of Revolut account |

|---|---|

|

|

Charles Schwab Global Investment Account

Charles Schwab offers a global account you can pair with a Schwab One brokerage account, to extend your investment options and pay in foreign currencies rather than USD. You can invest in 7 currencies and 12 of the top-traded foreign markets with the Global Investment Account, and trade online easily whenever you want to. Broker assisted trades are also available.

Best features of the Schwab account:

- No maintenance fees and no minimum balance

- Invest in 7 foreign currencies so you don’t need to switch back to USD between trades if you don’t want to

- Online and broker assisted services

How to open a Charles Schwab Global Investment account?

To open a Charles Schwab Global Investment account, you’ll need to already be a Schwab Brokerage customer to immediately start trading global products. To apply you can either call them on 800-992-4685 or via the Schwab website.

Eligibility for opening an account: To be eligible for a Charles Schwab Account you’ll have to be over 18 years of age and a US resident. You’ll also need to have a Schwab brokerage account.

| Pros of Schwab account | Cons of Schwab account |

|---|---|

|

|

HSBC Global Money Account

If you’ve already got an HSBC USD account you can also add in the HSBC Global Money Account to make it easier to hold and exchange 7 foreign currencies. HSBC offers competitive exchange rates, and you can then hold a foreign currency balance or withdraw your funds back to an HSBC account in your own or someone else’s name.

Best features of the HSBC account:

- Hold and exchange 7 global currencies

- Manage everything from the HSBC app

- No fee to transfer money back to an HSBC account

How to open an international account with HSBC

If you already hold an eligible HSBC account and have a US residential address, you can apply for an HSBC Global Account online. To get started, you’ll need to be registered for HSBC online banking and have their mobile app installed on your phone or tablet.

Eligibility for opening an account:

Anyone wanting to open an HSBC Global Account will need to already hold one of the following accounts: HSBC Premier Checking, HSBC Premier Savings or HSBC Premier Relationship Savings. You’ll also need a current US residential address.

| Pros of HSBC account | Cons of HSBC account |

|---|---|

|

|

Is it safe to keep money in international accounts?

All of the providers we’ve profiled are safe to use and comply with the required legislation to offer services in the US, and often, internationally, too.

- Wise: globally licensed and regulated, with strong digital security features

- Revolut: US services offered in partnership with Community Federal Savings Bank

- Charles Schwab: Safe banking brand – it’s useful to know brokerage products aren’t FDIC insured

- HSBC: large and trusted banking brand which is globally regulated

How much does it cost to open an international account?

Opening an international account is usually free, making international banking more accessible, but will vary from provider to provider. But even if an international account is free to open, it’s also important to be aware of other potential costs that could arise, like yearly or monthly maintenance fees, transaction fees or currency conversion charges. We’ll delve deeper into the important fees to consider in the next section.

Fees for opening an international account

Opening an international account is usually free of charge. However, different accounts do have their own fees, which can include maintenance fees. Some accounts may also require you to make and maintain a minimum deposit amount to access features and services.

Finally, international accounts from banks might also be available only to eligible customers who hold a USD account already with that bank – so you’ll need to double check if there are any fees involved in maintaining the USD account too, before you decide which international account to pick.

| Account fees | Wise account | Revolut account | Charles Schwab Global investing account | HSBC Global money account |

|---|---|---|---|---|

| Account opening fee | No fee | No fee | No fee | No fee |

| Minimum balance requirement | None | None | None | None |

| Fall below fee | None | None | None | None |

| Monthly or annual fees | None | No annual fees Monthly fees dependant on your chosen plan from $0-$16 per month | None | None |

| Account closing fees | None | None | None | None |

| Foreign transaction fees | No foreign transaction fee | No foreign transaction fee | Not stated on the website | No foreign transaction fee |

| Linked debit card fees | 9 USD order fee | No-fee with your chosen plan | Debit card not available | Debit card not available |

- Wise account – No fees for account opening, minimum balance or monthly maintenance charges. One-time 9 USD fee for ordering a linked debit card but no foreign transaction fees.

- Revolut account – No-fee for account opening but monthly maintenance fees are dependent on your chosen plan from $0 – $16 USD per month. There are no foreign transaction fees and you’ll receive a linked debit card with no delivery fee.

- Charles Schwab Global Investing Account – No fee to open an account and no minimum balance or fall below fee. The account doesn’t come with a linked debit card and there are no monthly or closing fees.

- HSBC Global Money Account – Open the account for free with no maintenance, closing or minimum account balance fees. There are no foreign transaction fees but the account doesn’t come with a debit card option.

How long does it take to open an international account?

The time it takes to open an international account can vary significantly from provider to provider and can range from a few hours to several days. While the application process tends to be straightforward, the verification process can take a while, ensuring that all mandatory security and regulatory compliance checks are done to securely set up your account.

Wise – Registration can take minutes but the verification process usually takes around 2 working days.

Revolut – Opening a personal account takes minutes but verification can take up to 7 business days in some cases.

Charles Schwab – Offers a relatively quick signup process, with online account applications taking on average 10 minutes. Verification timeframes aren’t specified but could take several hours to several days.

HSBC Global Money Account – As the account requires customers to already have an eligible HSBC account who have already gone through the initial verification process, opening a Global Money Account via the HSBC app should only take a few minutes.

Opening an international bank account online free with zero balance

While opening a free online international bank account with zero balance is possible, major banks often require a minimum deposit amount, which can be high for foreign currency accounts dealing in various currencies.

However, digital platforms like Wise and Revolut have made the process easy, quick and convenient, making it ideal for those who frequently travel or send and receive payments in multiple currencies.

With Wise you can hold, send and exchange over 40 currencies and gain access to up to 10 local account details, all without a minimum balance and no yearly or monthly fees. Revolut also doesn’t require a minimum deposit and supports over 25 currencies alongside the option of a no-fee monthly plan. Although customers will have to choose a plan with a monthly fee if they want to unlock additional account features and benefits like travel perks and unlimited no-fee currency exchange.

Tips for saving money with an international account

Here are a few extra ideas to help you get the most out of your international account:

- Avoid unnecessary currency exchange – if you’re paid in a foreign currency you can hold it in that currency instead of switching back to USD unnecessarily

- Get better rates – buy currencies you need when the rates look good, and hold the balance until you need it

- Avoid foreign transaction fees – international accounts often let you spend foreign currencies for free with no additional charge to worry about

How to open a foreign bank account online

If you’re interested in opening a bank account in another country online, from the US, our comprehensive guides for bank accounts in other countries can help:

- How to open a bank account in Australia 🇦🇺

- How to open a bank account in Canada 🇨🇦

- How to open a bank account in China 🇨🇳

- How to open a bank account in Europe 🇪🇺

- How to open a bank account in France 🇫🇷

- How to open a bank account in Germany 🇩🇪

- How to open a bank account in India 🇮🇳

- How to open a bank account in Japan 🇯🇵

- How to open a bank account in Mexico 🇲🇽

- How to open a bank account in the United Kingdom 🇬🇧

Can I open a bank account in another country without living there?

Non-US citizens can still open a bank account in the US, although the process can be more challenging, and they might need to go through some extra steps that citizens wouldn’t, especially if they’re non-residents. This often involves providing extra documentation, but specific requirements will vary depending on the bank and country.

Thanks to digital banking platforms like Wise and Revolut, opening a bank account in another country without being a resident there is much more accessible.

Wise offers the convenience of local bank details in up to 10 currencies, including USD, GBP, EUR, AUD, NZD, and CAD, allowing you to receive local transfers from over 30 countries as if you had a local bank account. For example, if you open a CAD account, you will get Canadian bank account details, effectively allowing you to bank like a local. Revolut personal accounts can be opened by legal residents of the UK, the EEA, Australia, Canada, Singapore, Switzerland, Japan and the US and also streamlines the process of managing money across borders, offering support in over 25 currencies.

Conclusion: International bank account opening

Ultimately the best bank for your international bank account will depend on your personal preferences and needs. US banks don’t usually have such a broad range of international account products for personal customers. Investors and businesses are better served, but you’ll need to shop around to find a bank and account that suits you.

Alternatively, specialist providers like Wise and Revolut can offer more flexible international account options which can hold dozens of currencies and which come with extra perks like low cost international transfer and currency conversion which uses the mid-market rate.

How to open an international bank account FAQs

What’s the best bank to open an international account in the US?

Banks in the US don’t usually offer a very broad selection of international accounts – although global brands like HSBC may be able to help. Alternative providers like Wise and Revolut may be a better option if you’re looking for a more flexible international account which has a good selection of supported currencies.

Can I open an international account online?

You can open an international account online or through an app if you pick a digital provider like Wise or Revolut. If you’d prefer to use a bank you may be eligible for online account opening if you’ve got a full set of standard documents available for verification – if not you’ll need to visit a branch.

What’s the bank with the cheapest international fees?

Banks tend to have fees for international transfers, overseas spending and currency exchange. While bank international fees can vary widely, customers often find they can access lower international fees by picking a specialist online service for their foreign currency transactions instead.

How much does it cost to open an international account?

It’s often free to open an international account, although some account providers do have maintenance fees. Transaction fees usually apply when you use your account, including currency conversion charges and ATM fees. Related: Best no-fee accounts in the US

Is it safe to keep money in an international account?

As long as you pick a reputable and properly licensed provider, it’s safe to keep money in an international account. All the providers we profile on Exiap are regulated and safe to use.

Sources: